Exemptions under the head of Salary Income as per Budget 2017 Plus All in One TDS on Salary for Non-Govt employees for the Financial Year 2017-18

Download Automated All in One TDS on Salary for Non-Govt employees for F.Y.2017-18 & A.Y.2018-19 [ This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Non-Govt Salary pattern + Automated H.R.A. Exemption Calculation + Automated Form 12 BA + Automated Form 16 Part A&B and Form 16 Part B with all the amended by the Finance Budget 2017-18]

|

Main Deductor's Sheet

|

|

Income Tax Computed Sheet

|

|

House Rent Exemption Calculator

|

|

Form 12 BA

|

|

Form 16 Part B

|

|

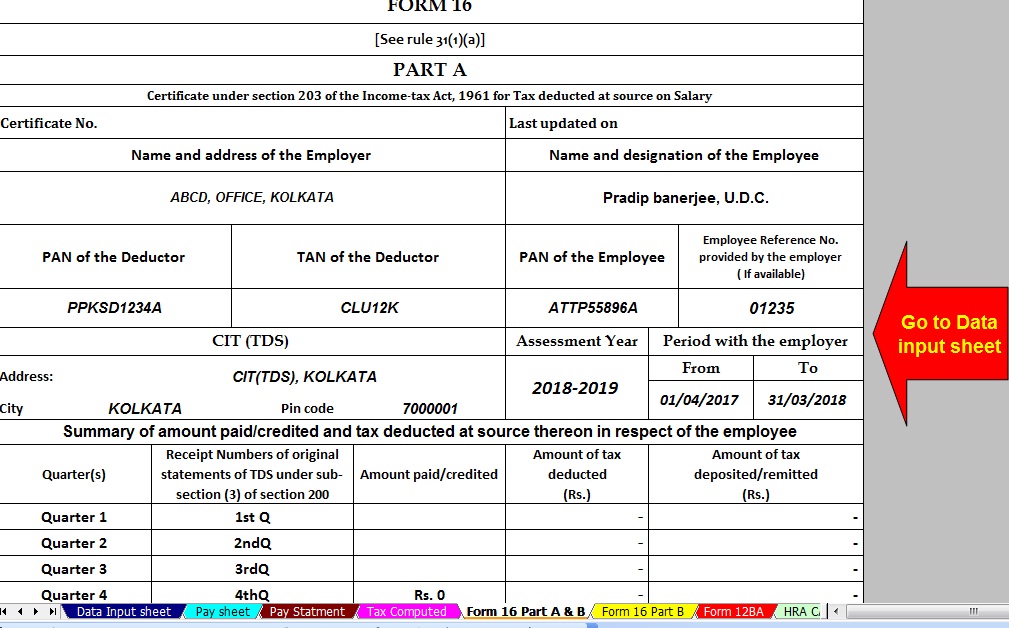

Form 16 Part A&B

|

Section - 10 (5)

Exemption for Leave Travel Concession

The amount actually incurred on the performance of travel on leave to any place in India by the shortest route to that place is exempt. This is subject to a maximum of the air economy fare or AC 1st Class fare (if the journey is performed by a mode other than air) by such route.

The amount actually incurred on the performance of travel on leave to any place in India by the shortest route to that place is exempt. This is subject to a maximum of the air economy fare or AC 1st Class fare (if the journey is performed by a mode other than air) by such route.

Provided that the exemption shall be available only in respect of two journeys performed in a block of 4 calendar years.

Section - 10(10):

Gratuity Exemption

Descriptions :

Least of the following will be exempt

1. Amount received

2. Max Rs. 10,00,000

3. 15*/26 x LS x (CYS + Fraction 6 months)

LS: Last Month Salary Drawn (Salary means Basic + DA (both))

Section - 10(10):

Gratuity Exemption

Descriptions :

Least of the following will be exempt

1. Amount received

2. Max Rs. 10,00,000

3. 15*/26 x LS x (CYS + Fraction 6 months)

LS: Last Month Salary Drawn (Salary means Basic + DA (both))

Section - 10(10AA)

Leave Encashment upon Retirement

Other Employee Least of the following will be exempted

1.Amount Received

2.Rs. 3, 00,000

3.10 x AS

(LE or 30 days) Received by Employee During the Employment (Fully TAXABLE)

Note - Govt. Employee {Fully Exempt} Received by Legal Heir (Fully exempt)

Section - 10(13A)

HRA

The least of the following will be exempted

1.Amount received

2.50% or 40% of Salary

3.Rent paid less 10% of Salary

4.Salary means; Basic Salary +D.A

Section - 10(14)

Children Education Allowance.

Rs.100 per month per child up to a maximum 2 children.

Hostel expenditure Allowance on employee’s child

Rs.300 per month per child up to a maximum two children.

Note: Allowance granted to meet Hostel expenditure Allowance on employee’s child.

Deductions under section 80 of Income Tax Act:

Section - 80C:

General deduction for investment in PPF, PF, Life Insurance, ULIP, Stamp duty on the house, Fixed deposits for 5 years, bonds etc. Maximum Rs. 1,50,000 is allowed. Investment need not be from taxable income.

Section - 80CCC

Deduction in case of a contribution to pension fund. However, it should be noted that surrender value or employer contribution is considered income. Maximum is Rs 1,50,000.

Section - 80CCD (1):

Deduction in respect to contribution to the new pension scheme. Employees of central and others are eligible.

The maximum is a sum of employer’s and employee’s contribution to the maximum: 10 % of salary.

Section - 80CCD (2): Employer’s Contribution to the Employees Pension Fund. This section is Additional deduction out of U/S 80C Limit Rs. 1.5 lakh.

Section - 80CCD (1B): Additional Deduction can be availed Max Rs.50 thousand to the New NPS Scheme, this deduction also allowing as Additional Deduction out of U/s 80C Max Rs.1.5 Lakh.

Section - 80CCE

It should be noted that employer contribution is allowable as extra u/s 80CCD(2) & 80CCD(1B) of the Income Tax Act from Asst YR 2018-19 and only employee's contribution is within limit of Rs 1 Lakh as stated in 80CCE

It should be noted that as per section 80CCE, the maximum amount of deduction which can be claimed in.

Section - 80D

Medical insurance on self, spouse, children or parents. The deduction is also allowable for CGHS contribution to Central and State scheme. It is also for conducting health check up to Rs 5000.

Rs 25,000 for self, spouse & children. IF parents are above 60 years, extra sum should be read as Rs 30,000. Thus maximum is RS 55,000 per annum to a person of age below 60 yrs.

Section - 80DD

For maintenance including treatment or insurance the lives of physical disable dependent relatives

Rs 50,000. In case of disability is severe, the amount is Rs 1,50,000. Watch video on 80DD Deduction

Section - 80DDB

For medical treatment of self or relatives suffering from a specified disease. The actual amount paid to the extent of Rs 40,000. In a case of a patient being Sr Citizen, an amount is Rs 80,000.

Section - 80E

For interest payment on loan is taken for higher studies for self or education of spouse or children. The actual amount paid as interest and start from the financial year in which he /she starts paying interest and runs till the interest is paid in full. Watch the video on 80E.

Section - 80EE

Interest on home loan sanctioned during F. Y. 2017-18. Maximum Rs 50 Thousand. The value of the property should be below Rs 50 Lakh and max loan sanctioned should be Rs 25 lakh. Further Assessee should not have any other residential house.

Section - 80G:

Donations to the charitable institution. 100% or 50% of an amount of donation made to 19 entities (National defense fund, Prime minister relief fund etc). For Asst Yr 2018-19, National Children Fund will also get 100% deduction.

Section - 80GG

For rent paid. This is only for people not getting any House Rent Allowance. Maximum is Rs 5000 per month or Rs.60,000/- P.A.

Section - 80TTA

Individual & HUF having interest in Savings Bank Account Rs 10,000 maximum Limit

Section - 80U

Deduction in respect of permanent physical disability including blindness to taxpayer

RS 75,000 which goes to Rs 1,50,000 in case taxpayer is suffering from severe disability.

Section - 87A

Rebate to an individual having low taxable income, Amount of tax or Rs 2,500 who’s taxable Income Less than 3.5 Lakh.

Deduction in respect of permanent physical disability including blindness to taxpayer

RS 75,000 which goes to Rs 1,50,000 in case taxpayer is suffering from severe disability.

Section - 87A

Rebate to an individual having low taxable income, Amount of tax or Rs 2,500 who’s taxable Income Less than 3.5 Lakh.

No comments:

Post a Comment